From Sputnik to Supply Chains: China's AI Vision

Beyond the arms race: China’s blueprint for embedding, not just surpassing

During my studies and before joining Alpha Intelligence Capital (global AI-focused VC1), I closely followed China’s geopolitical dynamics and technological trajectory. Over the past year, it’s become increasingly clear that the Western lens on China’s AI strategy often misses the deeper picture. The divergence isn’t just about technical prowess: it’s about fundamentally different assumptions around risk, scale, and timing.

Yes, China is investing heavily in foundational models. Companies like Deepseek, Moonshot, Zhipu, and 01.AI are making rapid progress. But history has proven that China’s real strength tends to emerge not at the bleeding edge of invention, but when technologies begin to plateau. Once the frontier stabilizes - once last year’s model becomes “good enough” for most use cases, China’s machinery kicks in: manufacturing scale, commercial adaptability, industrial integration, and fast iteration across a massive domestic market. It’s not about being first, it’s about saturating the stack.

As venture capitalist David Li put it - quoted by Dennis Kallin: “China builds arenas for the Hunger Games”. The phrase captures the dynamic well. Unlike Silicon Valley’s open-ended AGI ambitions, Beijing’s AI ecosystem functions more like a controlled tournament: ruthless internal competition, orchestrated state support, and intense pressure to commercialize early. Interestingly, The Economist recently reported that Chinese AI researchers “tend to place AGI further out on the calendar than their American peers”.

If Washington still channels Cold War instincts - betting on decisive breakthroughs to secure dominance, Beijing has drawn a more pragmatic lesson from history. The Soviets put the first satellite in orbit, but the U.S. turned its tech edge into broad industrial mobilization. What haunts Beijing isn’t Sputnik - it’s Gorbachev. Xi Jinping’s AI strategy reflects that anxiety. AI is less so treated as a moonshot, but as industrial life-support: a way to sustain productivity, mitigate demographic pressure, and preserve regime stability as internal pressures mount.

And yet, much of the Western debate still misreads the nature of this contest. It’s not simply a race to top chatbots & reasoning benchmarks. For Beijing, it’s a race to build politically resilient, economically self-sustaining AI infrastructure - systems that can scale, stabilize, and embed. In that game, durability often beats disruption.

We see too many of these…

…and not enough of those:

To understand China’s AI strategy, we need to unpack its core pillars: talent and data, industrial integration, nationwide infrastructure deployment, macroeconomic imperatives, and its long-term endurance doctrine.

The Iron Triangle: Talent, Data, and Policy

Morgan Stanley describes China’s AI ecosystem as powered by an "Iron Triangle": talent density, data abundance, and policy coordination.

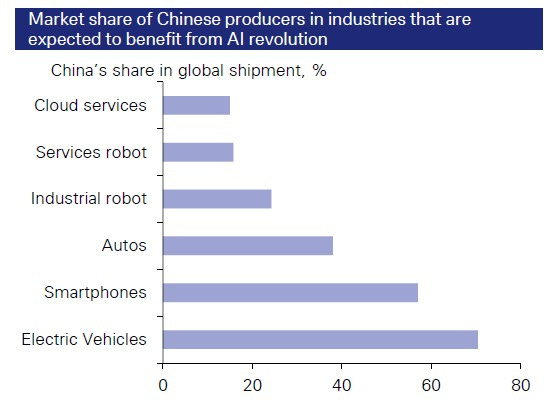

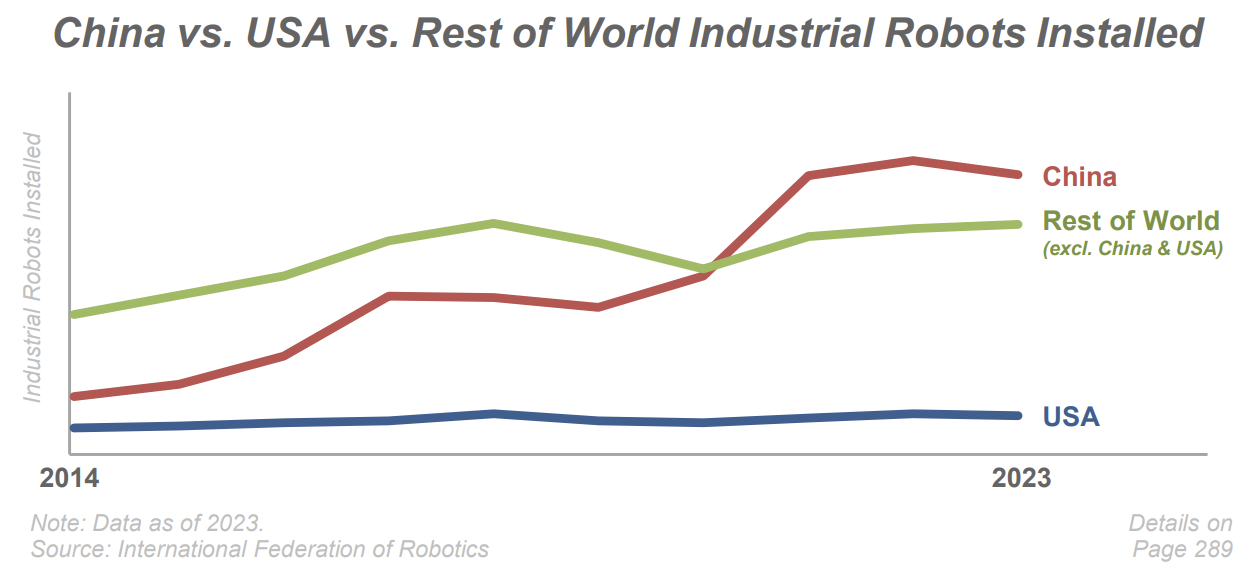

On talent, China now trains a staggering volume of AI engineers. Tsinghua University alone has spun out over 200 AI startups. Nearly half of global AI research papers and patents now originate from Chinese institutions. But where China stands apart is not merely academic publication - it is engineering deployment. Companies like BYD employ over 100,000 engineers, roughly so the total FTE headcount of Tesla. These engineers aren't optimizing language models; they're embedding AI into every conceivable industrial workflow: from EV assembly lines to logistics routing to predictive maintenance in state-owned enterprises.

China’s data advantage extends far beyond consumer platforms. Super apps like WeChat, Alipay, and Meituan collect multimodal user data at staggering scale. ByteDance alone processes over 80 million new video uploads daily. This gives Chinese firms rich, continuously updating training corpora for LLM fine-tuning, agent development, and cross-domain AI deployments. Crucially, this isn’t just about volume, it’s about usability. China’s population, including older demographics, is deeply fluent in app-based transactions across healthcare, banking, and public services. From triage booking to grocery delivery, these experiences are not just digital, they’re natively optimized, feeding AI systems with dense behavioral data and enabling real-time feedback loops.

But perhaps the most underestimated component is policy. China’s AI policy is vertically aligned, adaptive, and often brutally efficient once a strategic priority is set. Over 50 national AI standards have already been issued, provinces compete to launch AI+ manufacturing zones, and municipalities rapidly adopt AI-native public services with top-down coordination.

Two-Chain Integration: Merging R&D with Industrial Application

One of the key slogans emerging from Beijing’s AI doctrine is “创新链和产业链融合” or "innovation chain and industrial chain integration". Rather than view AI as a distinct research sector, China sees it as an accelerant to its industrial machine.

This model builds upon decades of supply chain dominance. The same factories that mass-produce smartphones, EVs, and drones are now modular platforms for rapid AI deployment:

LIDAR units designed for self-driving cars are retooled for port automation.

Drone batteries power off-grid AI compute stations.

EV motor controllers drive humanoid robots now being prototyped for warehouse operations.

Deutsche Bank describes this system as "cross-industry innovation" where AI is treated as a combinatorial upgrade to existing manufacturing moats. China's manufacturing depth becomes not just a hardware advantage but a flexible substrate for AI prototyping.

Xi Jinping himself has articulated this vision clearly: AI should be treated as infrastructure, like electricity, not as an atomic breakthrough akin to nuclear arms. It is not about shocking the world; it is about saturating every node of the economy.

The AI+ Initiative: Full Stack Deployment

This approach is now formalized under the “AI+ initiative” (人工智能+), a sweeping policy to integrate AI into industrial and public service infrastructure. Examples already deployed include:

Predictive maintenance systems using LLMs embedded in factory PLCs to reduce downtime.

Real-time logistics routing optimizing multimodal freight corridors.

AI-powered emergency triage systems embedded into rural clinic routers, enabling real-time health resource allocation.

AI-powered port operations increasing efficiency in shipping hubs.

But the picture is not without complications. Several analysts have raised concerns that this infrastructure-first approach risks premature technological lock-in. Embedding today’s LLM architectures too deeply into national infrastructure could create rigidity as frontier models continue to evolve rapidly abroad. China’s emphasis on cost-efficient, good-enough models may deliver immediate industrial gains, but may limit the adaptability needed for next-generation scientific breakthroughs.

The Three D's: AI as Macro-Economic Triage

China’s embrace of AI is not purely opportunistic; it is increasingly existential. As Zhou Jie (Tsinghua University) puts it “AI is being positioned as an industrial life-support system, not just for economic growth, but for social governance and national security.”

Beijing faces what economists describe as its "3D dilemma":

Deleveraging: The era of infrastructure-fueled credit expansion is over. Beijing's deleveraging campaign has constrained municipal debt issuance, forcing policymakers to seek new forms of productivity stimulus. AI-powered efficiency gains are being deployed to replace financial leverage with operational leverage.

Deflation: Chronic overcapacity and weak consumer sentiment risk long-term deflationary stagnation. AI is being positioned to create synthetic demand, from personalized education services to AI-generated entertainment content fueling new digital consumption niches. As Kexin Xu notes, the risk with AGI isn’t that it arrives too late for China - it's that its deflationary impact could exacerbate the very economic challenges Beijing is trying to offset.

Demographics: With its working-age population declining rapidly, China faces a looming labor shortage across sectors. AI-driven automation has become central to maintaining productivity, from robotaxi fleets (Pony.ai, Baidu) to warehouse & humanoid robotics and elder care assistants. That said, it's important to nuance this. Despite structural aging, China currently faces a labor surplus - especially among younger graduates and mid-career professionals. AI is not replacing labor due to immediate necessity, but rather as a forward-looking policy lever to prepare for future demographic shifts and realign mismatched labor markets.

Protracted War: The Endurance Strategy

No slogan better encapsulates China’s AI worldview than 持久战 (“protracted war”), originally articulated by Mao Zedong. The doctrine prioritizes systemic resilience over first-mover dominance.

Rather than focus on reaching theoretical AGI first, China is saturating every layer of its economic stack with "good enough" AI that compounds incrementally.

As Tsinghua’s Liu Zhiyuan puts it, "China’s AI strategy is not about outscaling the enemy, but outlasting them."

We’ve seen this before. In mobile internet, once payment systems and logistics tech matured, China didn’t need to out-innovate Amazon - it built Alibaba, Meituan, and a super-app ecosystem that integrated everything from messaging to delivery. In EVs, Tesla led with early breakthroughs, but once core technologies stabilized, China’s manufacturing scale and supply chain depth let companies like BYD pull ahead in production, cost, and exports.

The same dynamic may play out in AI. Once foundational models plateau, China’s edge shifts into gear. Its strengths are in turning good tech into great infrastructure: fast deployment, tight feedback loops, and massive market integration. That’s where the real advantage lies.

Yet this long-game approach reveals a central tension. The very apparatus that allows Beijing to coordinate national-scale deployments also tends to prioritize political insulation over adaptive flexibility. Rapid top-down execution may optimize for short-term industrial alignment, but often at the expense of decentralized experimentation, open intellectual debate, and the kind of frontier-disruptive research that thrives in looser systems. As Victor Shih notes, for the CCP, preserving centralized authority routinely overrides considerations of long-term economic optimality or scientific independence.

Conclusion: Lessons for Both Sides

The AI competition between China and the West is not a zero-sum race: it’s a contest between two fundamentally different development models. The West still dominates in foundational research, alignment science, and high-risk innovation. China is developing a model focused on scale, infrastructure, and adaptability, one that may ultimately prove more resilient, particularly in light of recent concerns about a slowdown in AI progress.

Western observers often frame China as lagging in innovation, but that framing misses the point. It’s not that China lacks technical ambition, companies like DeepSeek and Moonshot prove otherwise. It’s that China’s ecosystem is optimized for applied scale once the frontier matures.

The danger for the West is not just that China catches up in model performance. It’s that deployment at scale becomes its own flywheel, fueling data generation, fine-tuning, and productization in ways that slowly compress the capability gap. Alexandr Wang (ScaleAI) has warned that deployment/data is strategy. And in China, that logic is already policy.

Still, China’s system carries risks: lock-in to suboptimal architectures, political interference in capital allocation, and slower responsiveness to scientific disruption. Meanwhile, the U.S. and Europe are beginning to wake up, with industrial policy and infrastructure investments that suggest a pivot toward China’s playbook.

The real strategic question isn’t who dominates outright: it’s whether either system can absorb the other’s strengths before the next inflection point hits. Because in the end, the AI race won’t be won by reaching AGI first. It will be won by embedding intelligence into everything else - fast, cheap, and everywhere.

Sources

新华网. 大力推动我国人工智能大模型发展 (May 2025)

Artificial Analysis. State of AI: China Q1 2025.

World Economic Forum. Blueprint to Action: China’s Path to AI-Powered Industry Transformation 2025.

Morgan Stanley. China AI Playbook: The Giant Awakens (2025).

Deutsche Bank. The Upcoming AI Boom in China (March 2025).

MIT Technology Review. Manus Has Kick-Started an AI Agent Boom in China (June 2025).

The Economist. China’s AGI Doctrine: Pragmatism Over Moonshots (May 2025).

Victor Shih interview with Dwarkesh Patel. Xi Jinping’s Paranoid Approach to AGI, Debt Crisis, & Politburo Politics (May 2025).

Alpha Intelligence Capital invests globally, excluding Mainland China and the Greater China region.

The perspectives shared here are solely my own and do not reflect the views of Alpha Intelligence Capital.

Axel, really insightful and thought provoking article!

I generally agree that applications are the key, especially if we compete the adoption of digital technology in China vs Europe.

What is interesting in China is that the AI landscape is shifting with some companies like Deepseek, Stepfun and Moonshot focusing on AGI/research, while others like Baichuan and 01.ai start prioritizing applications. Do you see anything similar in other markets?

Also big question - how venture backable all the AI applications in China will be and what is the “moat”?